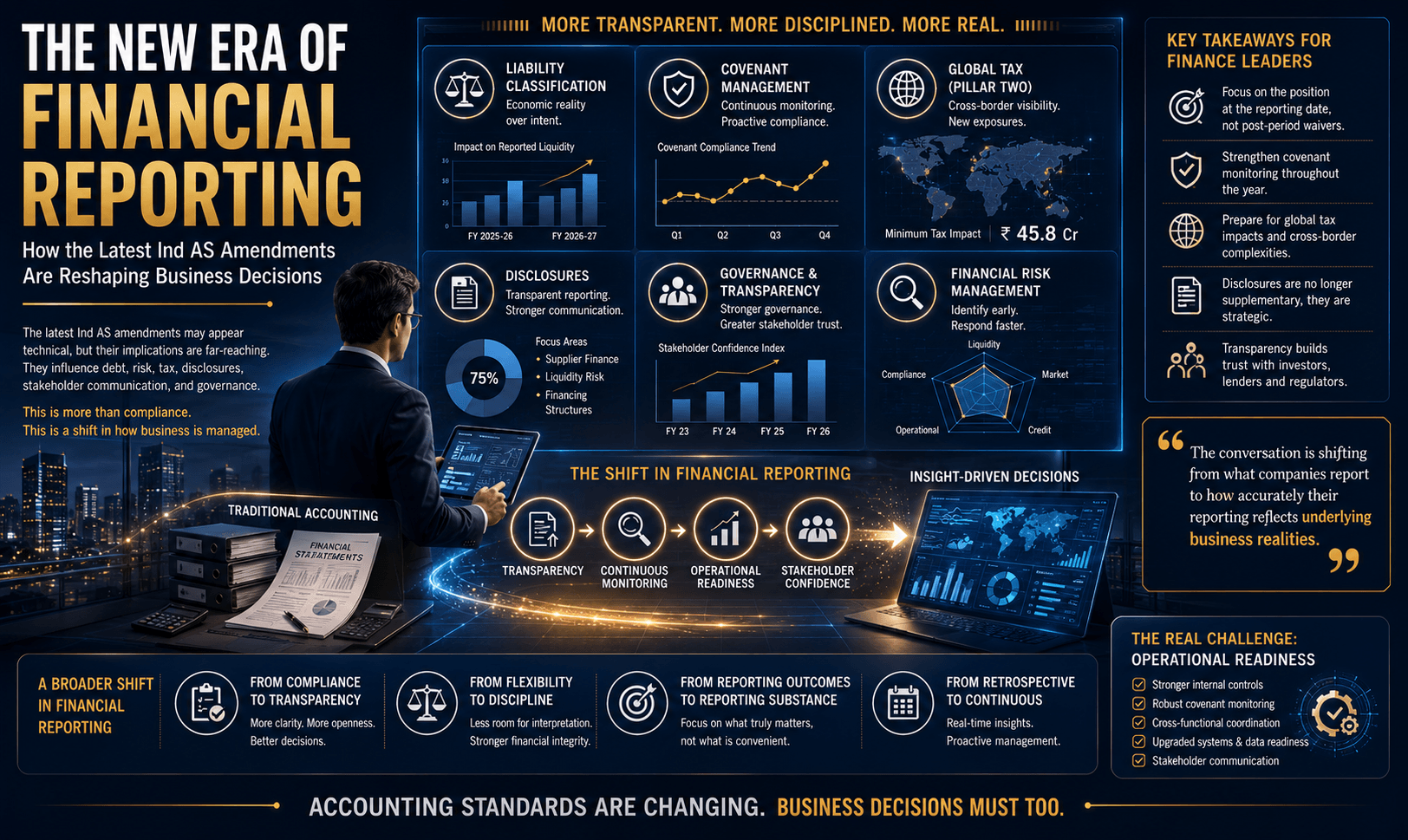

The latest Ind AS amendments may appear technical on the surface, but their implications extend far beyond accounting compliance.

These changes are set to influence how organisations manage debt, monitor financial risks, assess tax exposures, and communicate with investors and lenders. For finance leaders, the focus is shifting from technical interpretation to operational readiness.

While accounting standards are often viewed through a compliance lens, the latest amendments have implications that extend well beyond financial reporting. They influence liquidity management, financing decisions, tax planning, stakeholder communication, and governance practices.

Several developments stand out.

Liability Classification Is No Longer Open to Interpretation

One of the most significant changes relates to the classification of liabilities.

Beginning FY 2026-27, post-reporting date waivers from lenders will no longer influence whether a liability is classified as current or non-current. If an entity does not have the right to defer settlement of an obligation at the reporting date, the liability must be classified as current.

This places complete emphasis on the position that exists as of the balance sheet date rather than management’s expectations or subsequent developments.

For companies with structured debt arrangements, refinancing plans, or covenant-linked borrowings, the impact could be substantial. Reported liquidity positions may look materially different, even when long-term financing discussions are underway.

Covenant Management Must Become Proactive

The amendments also reinforce the importance of covenant monitoring.

Historically, some organisations could address covenant-related concerns through post year-end lender discussions and waivers. That flexibility is becoming increasingly limited. Classification outcomes will now depend on whether covenant requirements have been satisfied at the reporting date.

As a result, covenant compliance can no longer be viewed as a year-end exercise.

Finance leaders will need stronger monitoring mechanisms throughout the year, supported by regular dialogue with lenders and early identification of potential breaches. The objective is no longer simply resolving issues, but preventing them from affecting financial reporting outcomes in the first place.

Global Tax Is Becoming a Financial Reporting Consideration

The introduction of Pillar Two marks another important shift.

Tax is no longer solely a local compliance matter. Indian companies with international operations, as well as subsidiaries of multinational groups, may face tax implications that span multiple jurisdictions.

This creates new challenges around data availability, system readiness, and visibility across global operations. Organisations will need greater coordination between finance, tax, and technology functions to understand potential exposures and ensure accurate reporting.

For many businesses, this may require capabilities that extend well beyond traditional tax compliance frameworks.

Disclosures Are Becoming Strategic Decision Tools

Another notable development is the growing significance of disclosures.

Areas such as supplier finance arrangements, liquidity risk, and financing structures now require more transparent and meaningful reporting. Stakeholders increasingly rely on disclosures to understand the quality of earnings, resilience of cash flows, and the overall financial health of an organisation.

In this environment, the notes to accounts are no longer supplementary information. They are becoming an integral part of the financial story.

Investors, lenders, analysts, and regulators are paying closer attention to what organisations disclose, how they disclose it, and what those disclosures reveal about risk and governance practices.

A Broader Shift in Financial Reporting

Taken together, these amendments signal a larger transformation in financial reporting:

From compliance to transparency • From flexibility to discipline • From reporting outcomes to reporting substance • From retrospective assessment to continuous monitoring

The direction of travel is clear. Financial reporting is becoming more reflective of economic reality and less influenced by post-period adjustments or management intent.

The Real Challenge Is Operational Readiness

For most organisations, understanding the amendments will not be the difficult part.

The greater challenge will be ensuring operational readiness. This includes strengthening internal controls, improving covenant monitoring processes, enhancing cross-functional coordination, upgrading reporting systems, and preparing stakeholders for the impact of these changes.

The latest Ind AS amendments are ultimately about increasing transparency and strengthening confidence in financial reporting. Organisations that adapt early will be better positioned to navigate these requirements while providing stakeholders with a clearer and more reliable picture of their financial position.

In many ways, the conversation is shifting from what companies report to how accurately their reporting reflects underlying business realities. That is a significant change, and one that finance leaders cannot afford to overlook.