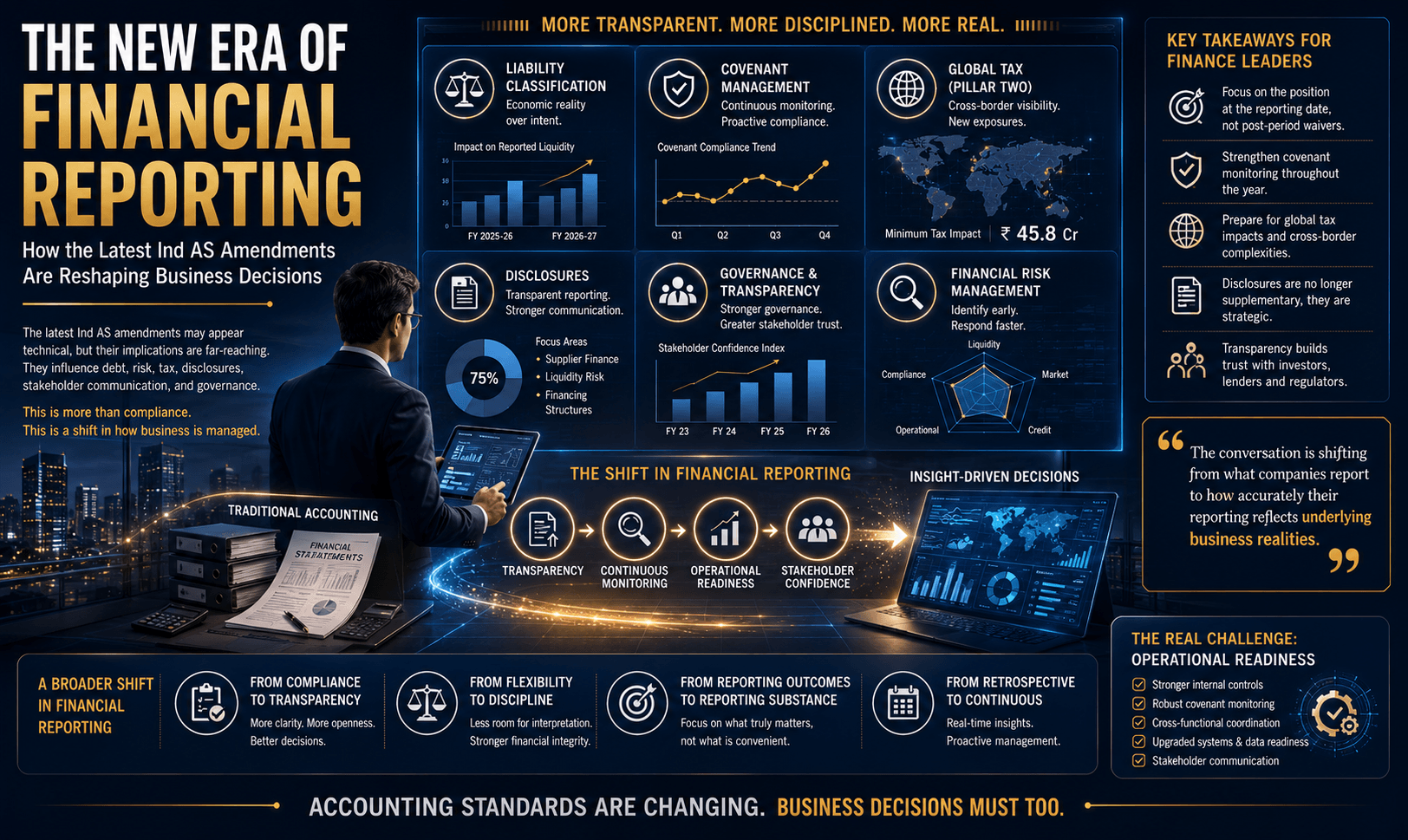

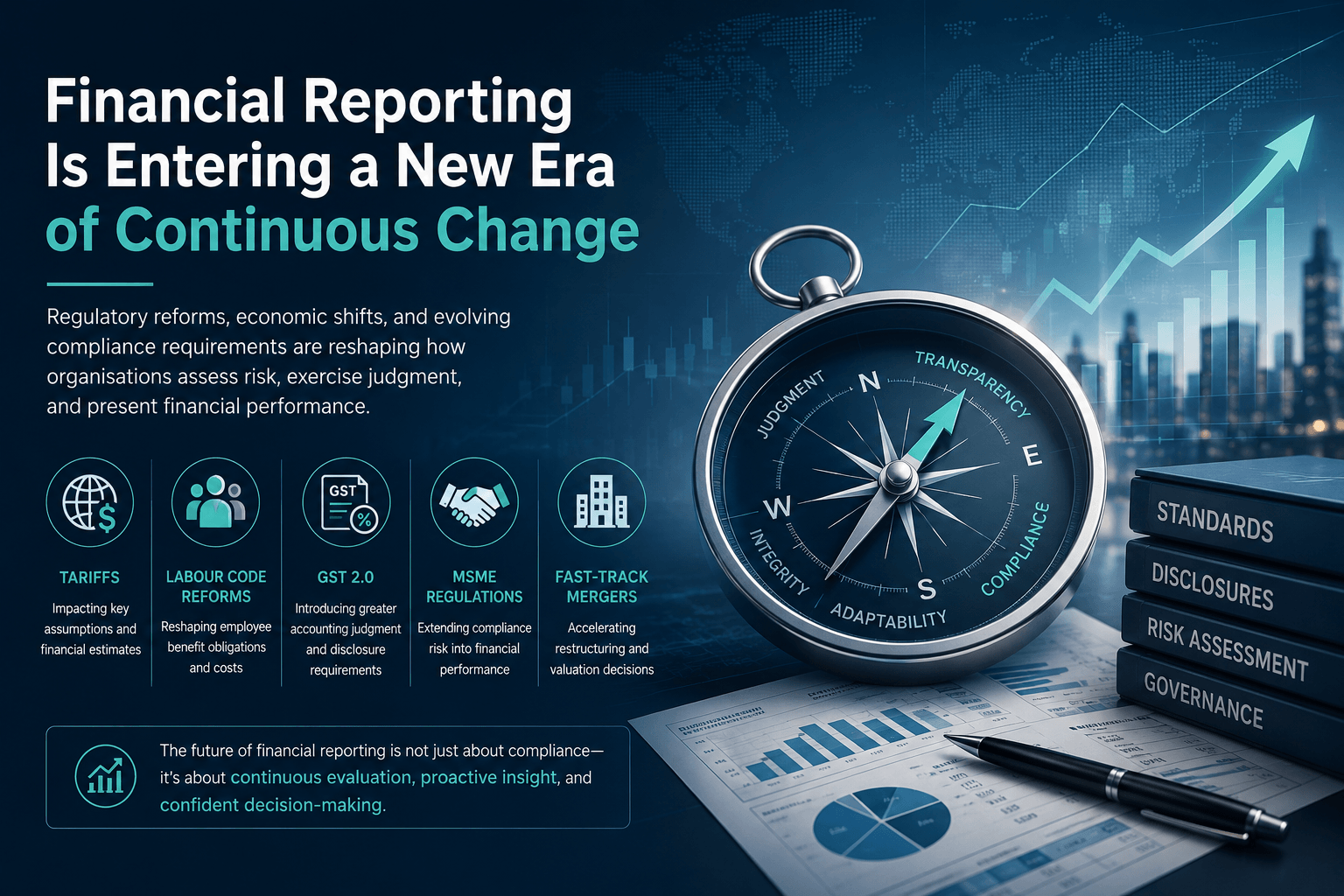

Financial reporting is undergoing one of its most significant transformations in recent years.

A combination of regulatory reforms, economic shifts, and evolving compliance requirements is forcing organisations to rethink how they assess risk, make judgments, and present financial performance. What were once considered external developments are now having a direct impact on financial reporting outcomes.

Financial reporting is no longer simply about applying accounting standards. It is increasingly about understanding how external developments affect business realities and ensuring those impacts are appropriately reflected in financial statements.

Several developments illustrate this shift.

Tariffs Are Becoming a Financial Reporting Variable

Changes in global tariff regimes are no longer confined to trade and supply chain discussions. They are beginning to influence key financial reporting areas, including impairment assessments, inventory valuation, revenue recognition, and expected credit loss calculations.

For businesses with significant cross-border exposure, assumptions around pricing, demand, profitability, and recoverability are becoming more volatile and increasingly dependent on management judgment. As trade dynamics evolve, organisations will need to revisit these assumptions more frequently and ensure that the rationale behind key estimates is adequately documented.

Labour Code Reforms Will Reshape Employee Cost Structures

The introduction of a uniform definition of wages and the expansion of gratuity-related provisions are expected to increase employee benefit obligations across many organisations.

The significance of these changes lies not only in their financial impact but also in their timing. These developments can trigger immediate recognition requirements under Ind AS 19, requiring companies to reassess employee benefit liabilities and reflect the impact within the same reporting period.

For finance leaders, this means evaluating workforce-related obligations proactively rather than treating them as a year-end exercise.

GST 2.0 Brings Greater Accounting Judgment

The next phase of GST reforms, including changes around Input Tax Credit (ITC) reversals and rate rationalisation, introduces accounting considerations that extend well beyond operational compliance.

Many of these changes create situations where more than one accounting treatment may be technically supportable. In such scenarios, consistency in application, robust documentation, and transparent disclosures become critical.

As tax regulations continue to evolve, organisations will need stronger coordination between finance, tax, and compliance teams to ensure reporting positions remain defensible and consistent.

MSME Regulations Are Extending Compliance Risk Into Financial Performance

Recent revisions to MSME thresholds and payment-related requirements mean that a larger supplier base now falls within the scope of MSME regulations.

As a result, payment delays are no longer merely operational concerns. They can have direct implications for tax deductibility and financial outcomes.

This development highlights the growing need for integration between procurement, finance, and compliance functions. Organisations that continue to manage these areas in silos may find themselves exposed to both regulatory and financial reporting risks.

Fast-Track Mergers Are Accelerating Restructuring Decisions

The introduction of simplified merger processes and reduced regulatory friction is making corporate restructuring more accessible and efficient.

This is likely to encourage greater consolidation activity across sectors. However, faster execution does not reduce the need for careful assessment of accounting, valuation, and disclosure implications.

Companies considering restructuring initiatives will need to ensure that financial reporting considerations are evaluated early in the decision-making process rather than addressed after transactions are underway.

A Broader Shift in Financial Reporting

Taken together, these developments point to a broader shift in the financial reporting landscape:

- From static standards to dynamic interpretation

• From siloed compliance to interconnected impact

• From year-end adjustments to continuous monitoring

• From periodic assessments to real-time decision support

The challenge for organisations will not be understanding individual regulatory changes. The real challenge lies in building the systems, governance frameworks, and cross-functional coordination needed to identify, assess, and respond to their implications as they emerge.

Financial reporting is increasingly becoming a forward-looking discipline. Organisations that invest in stronger processes, better data visibility, and proactive risk assessment will be better positioned to navigate this new environment.

The era of annual compliance-driven reporting is gradually giving way to one of continuous evaluation and dynamic interpretation. Finance leaders who recognise this shift early will be better equipped to manage uncertainty while maintaining transparency, credibility, and stakeholder confidence.