When I started advising on infrastructure projects nearly two decades ago, the financing conversation followed a fairly predictable script. You went to a public sector bank, negotiated a long-term loan, and then spent the next several months hoping land acquisition would not derail your timeline before the monsoons arrived.

Risk sat with the government. Money came from the same few places. Results were uneven, and everyone knew why.

That world is gone. What has replaced it is something genuinely different, and in many ways more interesting to work in.

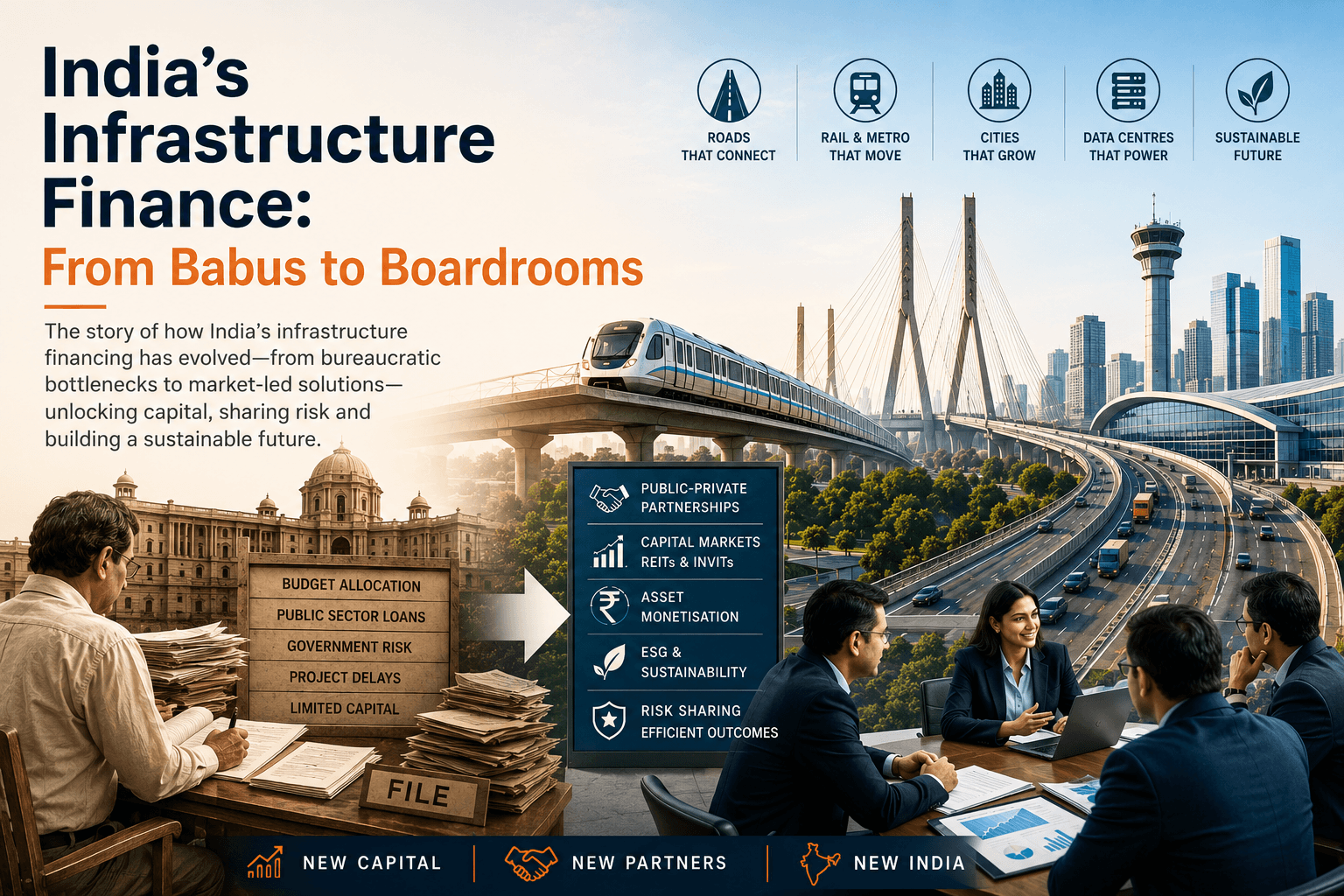

The old model and why it broke

For most of independent India’s history, infrastructure was a government affair. Roads came from budgetary allocations. Railways ran on sovereign borrowings. Power projects were financed through public sector banks that absorbed risk that was, frankly, not theirs to absorb.

Looking back, three fault lines defined that system.

First, banks were lending long against short-term deposits, a mismatch that was always going to create stress. Second, financial, operational and political risk was concentrated with one entity, the government. That concentration led to inefficiency and, eventually, inertia. Third, no government budget was ever going to keep pace with the scale of infrastructure India actually needed.

By the early 2010s, the system had buckled. Non-performing assets mounted. Projects stalled. It became clear that the architecture itself needed rethinking.

What has changed

The shift took time, and it is still unfolding, but the direction is unmistakable.

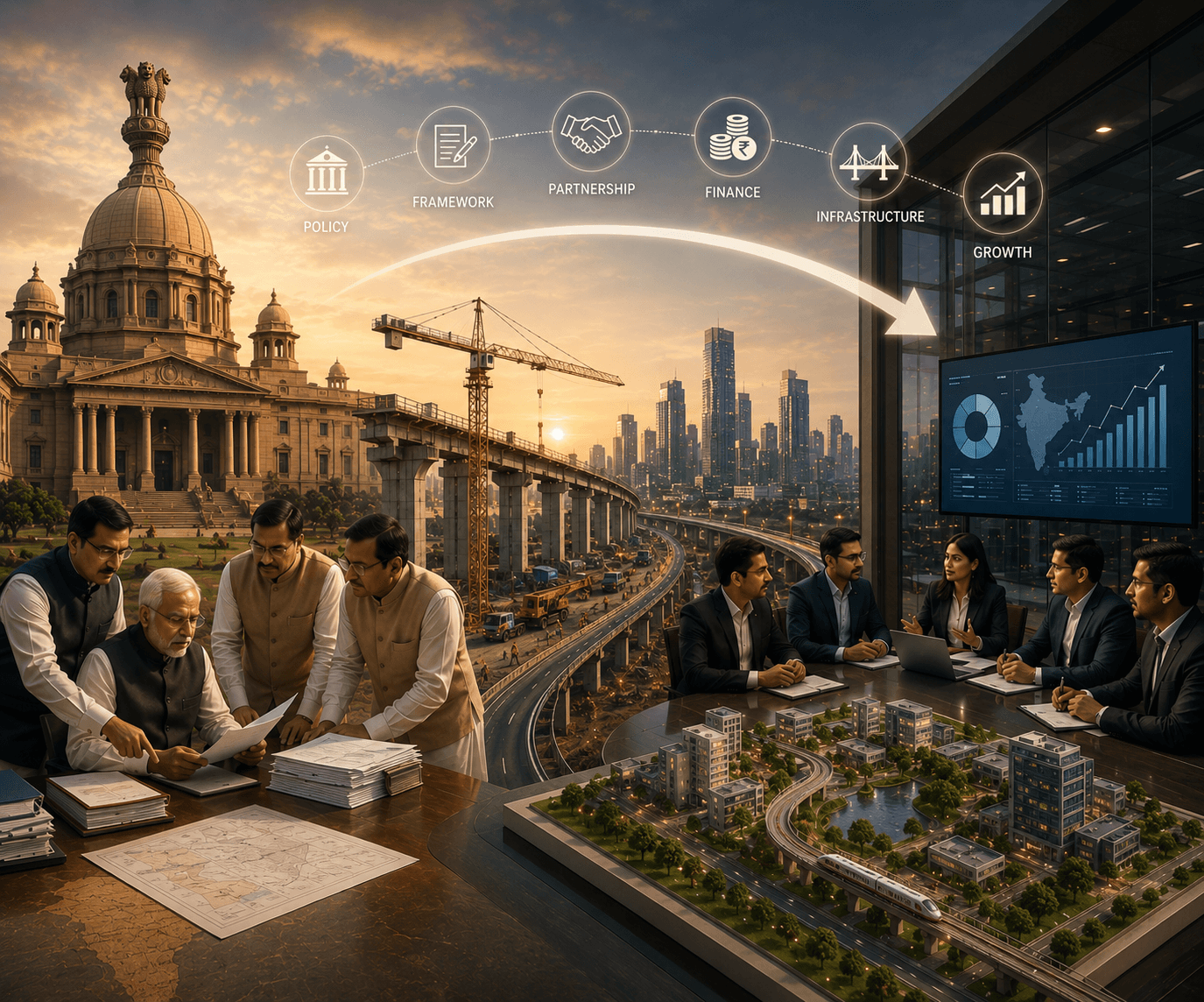

Public-Private Partnerships have moved from policy aspiration to operational reality. Build-Operate-Transfer, the Hybrid Annuity Model and Design-Build-Finance-Operate structures now define how roads, metro rails and airports get built. Risk is shared rather than concentrated, and that changes incentives across the lifecycle of a project.

In many of the projects I have been involved with, you can see this shift clearly.

Capital markets have entered the picture in a serious way. Infrastructure Investment Trusts and Real Estate Investment Trusts have created a new class of participants, retail investors, global pension funds and sovereign wealth funds, who now have a genuine stake in Indian highways and Grade-A office parks.

A decade ago, these were not assets you could invest in. Today, they are part of mainstream portfolios.

Governments have also started monetising what they already own. Rather than relying only on fresh borrowing, the approach now is to lease operational toll roads, airports and pipelines, use the proceeds to fund new projects, and recycle capital more efficiently.

And ESG considerations, once seen as peripheral, have quietly become central to investor decision-making. Green bonds and sustainability-linked frameworks are now part of how serious infrastructure capital is deployed.

What this means on the ground

Nowhere is the transformation more visible than in real estate and technology parks. The rise of REITs has opened access to Grade-A office assets that were once held almost entirely by institutions.

Cities like Bengaluru, Hyderabad and Mumbai are now investable markets for global capital in ways they simply were not before. Smart cities, data centres and fintech hubs have moved from aspiration to active deal flow.

Where we go from here

India’s ambition to reach a five-trillion-dollar economy rests, in significant part, on getting infrastructure finance right.

India does not have a capital shortage. It has a capital structure challenge.

Progress has been real. But the next phase will require deeper capital market development, stronger institutional capacity for contract management and dispute resolution, and policy consistency that gives investors the confidence to commit capital over long time horizons.

The babus are still in the room. So are the boardrooms.

The most interesting work now happens at their intersection.

What has your experience been with the changing infrastructure finance landscape? I would be glad to hear from developers, investors and policymakers in the comments.