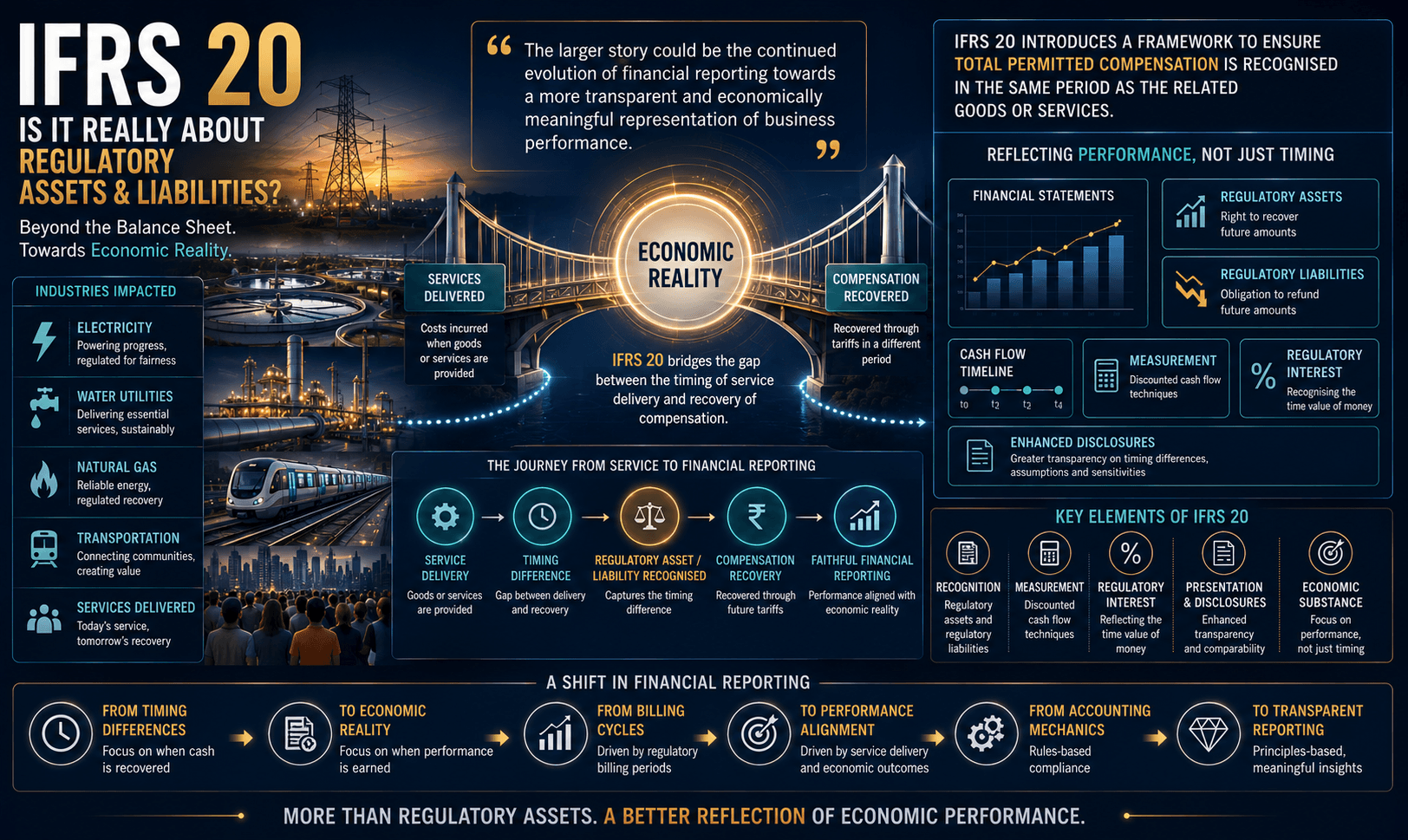

The issuance of IFRS 20, Regulatory Assets and Regulatory Liabilities, marks an important development in financial reporting for entities operating in rate-regulated industries. At first glance, the standard appears to focus on introducing a new framework for recognising regulatory assets and regulatory liabilities. However, a closer look suggests that its broader objective may be something more fundamental.

Financial reporting has increasingly evolved towards reflecting the economic substance of transactions and events rather than merely their legal form or timing. Viewed through this lens, IFRS 20 appears to be another step in that journey.

The Challenge of Timing Differences

Industries such as electricity, water, gas, and transportation often operate under regulatory frameworks that determine when and how costs can be recovered through customer tariffs.

In many cases, there can be a disconnect between the period in which goods or services are delivered and the period in which the related compensation is recovered. As a result, revenue recognised in a particular reporting period may not fully reflect the compensation associated with the services provided during that same period.

This timing mismatch can make it difficult for financial statements to present a complete picture of an entity’s performance.

How IFRS 20 Addresses the Issue

IFRS 20 seeks to bridge this gap by introducing regulatory assets and regulatory liabilities that capture these timing differences.

The objective is to ensure that total permitted compensation is recognised in the same reporting period as the related goods or services. By doing so, the standard aims to improve the alignment between operational performance and financial reporting outcomes.

The technical implications of the standard are significant and include:

- Recognition of regulatory assets and regulatory liabilities arising from timing differences

- Measurement using discounted cash flow techniques

- Recognition of regulatory interest

- Enhanced presentation and disclosure requirements

- Replacement of IFRS 14 and the introduction of a more comprehensive reporting framework

For affected entities, these changes will require careful evaluation of existing regulatory arrangements, measurement methodologies, and reporting processes.

Looking Beyond the Technical Requirements

What is particularly interesting about IFRS 20 is the philosophy underpinning the standard.

While the discussion often centres on the introduction of new balance sheet categories, the broader objective appears to be improving how financial performance is represented. The standard seeks to ensure that financial statements more faithfully reflect the economic consequences of providing regulated goods and services, even when billing and cash recovery occur across different reporting periods.

In that sense, regulatory assets and liabilities may be viewed as the mechanism through which a larger objective is achieved, namely, a more accurate representation of financial performance.

This aligns with a broader trend in financial reporting, where accounting standards increasingly focus on presenting economic reality rather than simply recording transactions based on their timing.

Preparing for the Transition

Although IFRS 20 becomes effective for annual reporting periods beginning on or after 1 January 2029, organisations should not underestimate the preparation required.

Identifying timing differences, evaluating enforceable rights and obligations, developing appropriate measurement models, and strengthening data collection processes will all require considerable planning and professional judgment.

For many entities, implementation will involve collaboration across finance, regulatory, operational, and technology functions to ensure a smooth transition.

More Than a New Accounting Standard

IFRS 20 is undoubtedly a technical standard. Yet its significance may extend beyond the creation of regulatory assets and liabilities.

At its core, the standard appears to reinforce a fundamental principle of modern financial reporting: financial statements should reflect economic performance as faithfully as possible, even when commercial, regulatory, and cash flow realities do not align neatly within a reporting period.

The new accounting requirements may attract the headlines, but the larger story could be the continued evolution of financial reporting towards a more transparent and economically meaningful representation of business performance.